Something has fundamentally changed in the gold market.

This isn’t another inflation scare. This isn’t another flight to safety that fades in a few weeks.

This is institutional capital repositioning on a scale we haven’t seen in decades.

Gold is nearing $5,000 per ounce.1 Silver is up over 150% year over year.

And the buyers driving this rally aren’t retail speculators chasing momentum. They’re central banks. Sovereign wealth funds. The kind of players who don’t buy gold because it’s going up. They buy it because they see what’s coming.

China has dumped US Treasuries to their lowest level in 17 years.2 At the same time, Beijing extended its gold-buying streak for 13 consecutive months.

Central banks globally have purchased over 1,000 tonnes annually since 2022. And 76% of them plan to keep buying.3

The message is clear. The world’s most powerful institutions are quietly exiting dollar assets and piling into hard money.

And they’re not alone.

Tether, the company behind the world’s largest stablecoin, has quietly accumulated 116 tonnes of physical gold.4 That’s over $5 billion in bullion. From a single buyer. In less than two years.

Meanwhile, Goldman Sachs is calling for $5,400 gold by Q4 2026.5 Bank of America sees gold prices hitting $6,000 by the spring.6

And one senior commodities strategist at ICBC Standard Bank sees gold prices pushing as high as $7,150.7

This is the setup. And it changes everything for gold producers.

Because when gold moves from $2,000 to $5,000, producers don’t just see revenues climb 2.5x. With operating leverage, margins may be able to expand 5x. Cash flow can potentially multiply 10x. That’s the math that turns juniors into billion-dollar companies.

But here’s the problem. There aren’t many new producers coming online.

According to BMO Capital Markets, only a handful of single-asset gold producers were set to launch in 2025. New supply is growing at just 1% annually.8 And most development projects are still years away from first pour, stuck in permitting, financing, or feasibility purgatory.

That’s what makes this story different.

Norsemont Mining Inc. (CSE:NOM) (OTCQX:NRRSF) isn’t building a mine from scratch. They acquired one.

In 2020, Norsemont acquired Chile’s third-largest historic gold producer. A project called Choquelimpie.9

Between 1988 and 1992, Shell extracted 398,900 ounces of gold and 2.19 million ounces of silver from this high-sulfidation epithermal system.10 Then they walked away. Gold was under $400 per ounce. The economics didn’t make sense.

But they left behind something remarkable.

A 3,000 tonne-per-day crushing plant, an ADR processing facility, power lines connected to the grid, water permits for 76 liters per second, year-round road access, a refurbished 35-person camp, warehouses, fuel tanks and a sample preparation lab.

Historical exploration activity includes over 2,000 drill holes, for 143,047 meters of drilling.11 Work and infrastructure that would cost $175 million to replicate today.12 Materials from this drilling are well-preserved on site and available to be utilized for additional studies.

Norsemont Mining (CSE:NOM) (OTCQX:NRRSF) didn’t spend a decade exploring. They didn’t raise hundreds of millions for construction. They stepped into a project with an estimated $175 million worth of infrastructure already built, already permitted, already waiting.

And now, with gold nearly 20 times higher than when Shell shut it down, they’re bringing the Choquelimpie project back online.

The production target is 2027. Just 18 to 24 months away.13

And with management targeting very low cash costs, the math gets very interesting very quickly at $5,000 gold price on a 30,000 to 35,000 ounce per year operation.14

This is the kind of setup that sophisticated investors spend years searching for. A past-producing asset. Existing infrastructure. A clear path to cash flow. In a tier-one jurisdiction. Led by a team that has already built and exited billion-dollar mining companies.

And it’s exactly why names like Rob McEwen, Paul Matysek, Quinton Hennigh, and Crescat Capital have been quietly accumulating shares of Norsemont Mining Inc. (CSE:NOM) (OTCQX:NRRSF) ahead of what could be a transformational year.15

8 Reasons

Norsemont Mining Could Be the Most Asymmetric Gold Opportunity of 2026

Not every gold junior is built the same.

Some are years away from even knowing what they have. Others are drowning in capex requirements and permitting timelines that stretch into the next decade. And most will never produce a single ounce.

Then there are the rare setups where the stars align. Where infrastructure already exists. Where the resource is already defined. Where the team has already done this before. Where the path to production is measured in months, not years.

Norsemont Mining Inc. (CSE:NOM) (OTCQX:NRRSF) checks every one of those boxes.

Here’s why this story deserves serious attention right now.

1

They Acquired Infrastructure That Most Juniors Spend a Decade Building : Choquelimpie, located in northern Chile, isn’t a greenfield exploration play. It’s a past-producing mine with a 3,000 tonne-per-day mill, power, water, roads, camp facilities, and 1,710 historical drill holes already in the ground. That infrastructure would cost approximately $175 million to replicate today.16 Norsemont acquired it all when they took over the project, giving them a massive head start that eliminates years of development risk.

2

Production Is Targeted for 2027, Not 2030 or Beyond: While most developers are still talking about feasibility studies and permitting timelines, Norsemont Mining (CSE:NOM) (OTCQX:NRRSF) is fast-tracking toward production with a target of 18 to 24 months. The oxide material is amenable to heap leaching. The plant infrastructure exists. The EIA process is already underway with a supportive regional government that has been actively encouraging the company to submit. This is a near-term production story in a market starving for new supply.

3

The Macro Timing Could Not Be Better: Gold just is testing $5,000 per ounce. Silver broke $115. Central banks are buying at the fastest pace in decades, and major institutions are forecasting $6,000 gold by spring. The NI 43-101 technical report used $2,500 gold and $28 silver for its resource calculations. At today’s prices, the economics of Choquelimpie are dramatically better than what’s on paper. Every dollar gold rises adds leverage to this story.

4

The Resource Has 3x to 4x Expansion Potential: The current resource stands at 2.18 Million indicated & 557,000 inferred gold-equivalent ounces. But here’s what most investors miss. The average historical hole was only drilled to a depth of 70 meters. High-sulfidation epithermal systems like Choquelimpie typically extend to 300 meters depth. Management is targeting 7.5 million to 9 million ounces by drilling deeper into known mineralization. They’re not hoping to find new zones. They’re proving that the zones they already have go much deeper than previously tested.

5

There’s a Copper Porphyry System at Depth That Could Change Everything: Beneath the gold-silver epithermal system sits something potentially much larger. A 2021 drill hole hit 170 meters grading 1.35 g/t gold, 18.3 g/t silver and 0.2% copper, with grades increasing to 0.7% to 1.1% copper at depth.17 Dr. Sergei Diakov, who was part of the team that discovered the massive Oyu Tolgoi deposit, joined Norsemont’s board specifically because of this porphyry potential.

6

The Smartest Money in Mining Is Already on the Register: This isn’t a story being funded by hedge funds and momentum traders. Norsemont Mining Inc. (CSE:NOM) (OTCQX:NRRSF) has raised over $21 million from some of the most respected names in the sector.18,19 Billionaire Rob McEwen. Serial entrepreneur Paul Matysek, who has sold multiple mining companies for billions. Quinton Hennigh and Crescat Capital, who built their reputation identifying undervalued gold stories. Victor Cantore of Amex Exploration. Macro investor Larry Lepard. And notably, Crescat increased their position at a higher price in December, a signal of conviction that’s hard to ignore.

7

The CEO Has $10 Million of His Own Money in This Deal: Marc Levy isn’t a promoter collecting a salary while shareholders take all the risk. He and his family trust have invested approximately $10 million into Norsemont, representing roughly 21% ownership of the company. Levy built the original Norsemont Mining from a $1 million market cap to a $520 million sale to Hudbay Minerals. He has been involved in over $1 billion in mining exits.20 When the CEO has that much skin in the game, interests are aligned.

8

The Valuation Disconnect Is Glaring: The standard industry rule of thumb values development-stage gold ounces at $100 per ounce. At 2.18 million indicated & 557,000 inferred gold-equivalent ounces,21 that implies a valuation around $300 million. Norsemont Mining (CSE:NOM) (OTCQX:NRRSF) currently trades at roughly $96 million market cap. That’s less than $40 per ounce for a past-producing asset with existing infrastructure, near-term production potential, resource expansion upside, and copper optionality at depth. For comparison, Rio2 is mining in Chile at lower grades with a market cap of $1.75 billion. The gap here is difficult to justify.

Inside Choquelimpie. The Past-Producing Gold Mine That Shell Built and Walked Away From With Millions of Ounces Still in the Ground

Some deposits take decades and hundreds of millions of dollars to understand.

Choquelimpie is not one of those deposits.

Shell built this into Chile’s third-largest gold producer in the late 1980s.

Between 1988 and 1992, they extracted 398,900 ounces of gold and 2.19 million ounces of silver through heap leaching before walking away when gold dropped below $400 per ounce.22

They didn’t leave because they ran out of gold. They left because the economics stopped working.

The gold never went anywhere. Neither did the silver. And neither did the copper mineralization that runs through the deeper parts of the system.

Norsemont Mining Inc. (CSE:NOM) (OTCQX:NRRSF) now controls 100% of this asset. And the updated NI 43-101 resource estimate published in May 2025 confirms exactly what’s still in the ground.23

Mineral Resource Estimate (March 31, 2025)

| Category | Tonnes (M) | Au (g/t) | Ag (g/t) | Cu (%) | AuEq (g/t) | AuEq Ounces |

| Indicated | 81.89 | 0.66 | 12.62 | 0.04 | 0.83 | 2,184,000 |

| Inferred | 25.27 | 0.55 | 8.89 | 0.04 | 0.69 | 557,000 |

Over 80% of those ounces sit in the higher-confidence Indicated category. That’s not a speculative inferred resource that may never convert to anything mineable. This is material that has been drilled, tested, and validated through decades of work and actual production.

Look at the indicated silver resource of 33 million ounces at an average grade of 12.6 g/t, plus the inferred resources of an additional 7 million ounces at an average grade of 8.9 g/t. With silver now trading above $100 per ounce for the first time in history, that’s not a rounding error.

That’s a meaningful credit that enhances the economics of every tonne mined. And the 0.04% copper running through the system adds yet another layer of value, particularly as the deposit extends deeper toward the porphyry source.

But the real story at Choquelimpie is what the historical operators left behind in the drill results.

Selected High-Grade Drill Intercepts

| Zone | Hole ID | From (m) | To (m) | Interval (m) | Au (g/t) | Ag (g/t) |

| Vizcacha | A-327 | 0 | 35 | 35 | 30.5 | 7 |

| Vizcacha | A-417 | 0 | 22 | 22 | 13.7 | 3 |

| Choque | R002 | 0 | 160 | 160 | 3.8 | 193 |

| Choque | R066 | 0 | 120 | 120 | 4.1 | 222 |

| Siri | R-554 | 96 | 154 | 58 | 6.4 | 167 |

| Siri | R579 | 2 | 26 | 24 | 35.1 | 137 |

That top Vizcacha hit of 35 meters at 30.5 g/t gold represents over 1,000 gram-meters. Anything over 100 gram-meters is significant. Over 1,000 is world-class territory.

And don’t overlook the silver in those Choque and Suri intercepts. Hole R-002 returned 160 meters at 193 g/t silver with the gold.24 R-066 hit 252 g/t silver over 120 meters. 25

At today’s silver prices, these intercepts carry substantial standalone value before you even count the gold. This is a true polymetallic system where gold drives the story but silver and copper provide meaningful economic uplift.

Here’s the critical insight most investors miss.

The average historical drill hole only went down 70 meters. But high-sulfidation epithermal systems like Choquelimpie typically extend to 300 meters depth. Shell stopped drilling while still in ore. Many holes ended in mineralization because they weren’t trying to define the full system. They were just chasing the easy near-surface material.

That’s why management believes this resource can grow from 2.18 Million indicated & 557,000 inferred gold-equivalent ounces to 7.5 million ounces or more. Not by finding new zones. By drilling deeper into zones that are already defined and already mineralized.

The gold, silver, and copper are down there. The historical drilling indicates the system is open at depth. Now it’s a matter of proving out the volume.

And Norsemont Mining Inc. (CSE:NOM) (OTCQX:NRRSF) isn’t starting from scratch. The project comes with hundreds of millions worth of infrastructure already built.

-

-

- A 3,000 tonne-per-day mill.

- Power connected to the grid.

- Water permits for 76 liters per second.

- Year-round road access. A refurbished camp.

- Core storage with historical drill hole material preserved.

-

Most juniors spend years permitting access roads and negotiating power purchase agreements. They raise hundreds of millions just to build basic infrastructure. Norsemont will skip all of that. They acquired a turnkey operation that Shell and Northgate spent tens of millions constructing in the 1980s.

That infrastructure is what separates Choquelimpie from the hundreds of other gold deposits sitting in development limbo around the world. It’s what makes a 2027 production target realistic instead of a pipe dream.

The asset is real. The infrastructure is real. The historical production proves the system works. Now it’s about executing the plan.

The Fast Track to Cash Flow. How Norsemont Plans to Be Pouring Gold in 2027 Without Raising Hundreds of Millions

Most gold developers measure their path to production in decades and billions of dollars.

Norsemont Mining Inc. (CSE:NOM) (OTCQX:NRRSF) is measuring theirs in months and tens of millions. Norsemont’s primary asset is Choquelimpie, a past-producing gold mine, located in mining-friendly Chile.

The target is commercial production in 2027. Not 2030. Not “sometime later this decade.” Eighteen to twenty-four months from now. And the capex to get there? With all of the infrastructure in place, management expects very low restart costs in the tens of millions.

Compare that to typical development projects requiring $500 million to $1 billion in construction capital, years of permitting delays, and complex project financing that dilutes shareholders into oblivion. The difference in execution risk is night and day.

Here’s how Norsemont plans to pull it off.

The fastest path to cash flow runs through the oxide material located near the surface. This is the same type of ore that Shell successfully mined and heap leached in the late 1980s. It doesn’t require complex metallurgy. It doesn’t require a massive processing plant. And a significant portion of it is already sitting in stockpiles on site.

Norsemont conducted 69 sonic drill holes across the historical dumps26 and identified approximately 196,000 gold equivalent ounces in material that fell below the cutoff grade when gold was $400 per ounce. At nearlt $5,000 gold, that material is now highly economic. It’s already mined. Ready to process.

Beyond the stockpiles, the company has identified an additional 244,000 ounces of gold in-place shallow oxide that can be brought into the production plan through targeted drilling.

The Environmental Impact Assessment (EIA) process is underway in a region that actively wants mining development.27 Chile’s Arica-Parinacota region has limited economic opportunity outside of resource extraction. Government officials have told Norsemont directly that they want this project to succeed. The typical EIA review period runs six to twelve months, making a 2027 production start achievable.

And here’s what makes this pathway so compelling. The oxide operation isn’t the end of the story. It’s the beginning.

Once cash flow starts, Norsemont Mining Inc. (CSE:NOM) (OTCQX:NRRSF) plans to self-fund expansion into the mixed and sulfide material representing over 1.6 million additional ounces. The capital for growth comes from operations, not dilutive equity raises.

Management has been clear about the vision. Start with oxides. Generate cash flow. Fund the growth internally. Build toward a large-scale copper-gold operation without handing the upside to investment banks.

That’s how you build a multi-billion dollar gold company. And it starts with the first pour in 2027.

Press Releases

- Norsemont Reports Significant Copper, Lead & Zinc Values in Three Choquelimpie Drill Holes

- Norsemont Resumes Phase Three Drill Program at Choquelimpie

- Norsemont Commences Trading on the OTCQX Market

- Norsemont Targets Filing Environmental Impact Declaration In December 2026

- Norsemont Invites Shareholders and Investment Community To Visit Us at Booth 3035 at PDAC 2026 in Toronto, March 1–4

The Resource Could Potentially Triple From Here. And Potential for a Copper Porphyry Hiding Beneath It That Could Change Everything

The current resource stands at 2.18 million ounces indicated and 557,000 inferred gold-equivalent ounces. That alone would be enough to build a meaningful gold company.

But management isn’t stopping there. They believe Choquelimpie holds 7.5 to 9 million ounces once the deeper zones are properly tested. And beneath all that gold and silver sits something potentially much larger.

A copper porphyry system that could potentially be worth multiples of the entire current market cap.

Here’s the logic behind the resource expansion.

The historical drilling at Choquelimpie averaged just 70 meters depth. Shell and Northgate were focused on shallow oxide material for heap leaching. They weren’t trying to define the full extent of the mineralized system. They were extracting quick ounces while gold prices supported the operation.

But high-sulfidation epithermal deposits like Choquelimpie don’t stop at 70 meters. They typically extend to 300 meters or deeper. The geological model suggests that Norsemont Mining Inc. (CSE:NOM) (OTCQX:NRRSF) is sitting on three to four times more gold simply by drilling down into zones that are already defined at surface.

This isn’t grassroots exploration hoping to stumble onto something. This is systematic infill and extension drilling into mineralization that has already been validated by historical production. The Phase 3 drill program currently underway is testing exactly this thesis with 20 diamond drill holes targeting 300 meter depths across the highest-priority zones.

And then there’s the copper.

In 2021, Norsemont drilled a hole (MV21-009) that changed the entire complexion of this project. At depth, they encountered 170 meters grading 1.35 g/t gold and 0.2% copper.28 More importantly, the copper grades increased as the hole went deeper, hitting 0.7% to 1.1% copper in the final intervals before they stopped drilling at around 300 meters.

Geologists recognized what this meant immediately. They may have hit the cupola, the top of a copper porphyry system.

This is the engine that drove all the gold and silver to surface in the first place. And it’s sitting right beneath the existing resource.

Dr. Sergei Diakov joined the Norsemont Mining (CSE:NOM) (OTCQX:NRRSF) board specifically because of this porphyry potential. Sergei led the team that discovered Oyu Tolgoi, one of the largest copper-gold deposits ever found. When he reviewed the Choquelimpie data, he told management they had a large copper porphyry system that needed to be tested.

The potential scale is significant. Management believes this could be a 500 million to 1 billion tonne target at grades approaching those of other Andean copper deposits. At those dimensions, you’re talking about a deposit that would attract interest from the world’s largest mining companies.

Norsemont Mining Inc. (CSE:NOM) (OTCQX:NRRSF) isn’t valued for any of this copper upside today. The market is pricing it as a gold development story. But if the porphyry proves out, this becomes something else entirely. A dual-asset opportunity where the gold operation funds exploration into a potentially world-class copper system sitting directly underneath.

That’s the kind of optionality that can potentially create a ten-bagger.

Follow the Money. The Smartest Names in Mining Are Already on This Register and They’re Not Selling

You can learn a lot about a company by looking at who’s buying the stock.

Momentum traders chase charts. Hedge funds flip positions. Retail investors pile in after the move has already happened.

But when billionaires, legendary mine builders, and the most respected funds in the gold sector all start accumulating shares in the same junior? That’s a different signal entirely.

Norsemont Mining Inc. (CSE:NOM) (OTCQX:NRRSF) has quietly assembled one of the most impressive shareholder registers in the junior mining space. And these aren’t passive holders waiting to dump on the next pop. These are long-term strategic investors who have done the due diligence and placed meaningful bets.

Rob McEwen is on the register. The billionaire founder of Goldcorp who built one of the most successful gold companies in history. When McEwen takes a position in a junior, people pay attention.

Paul Matysek is on the register. The serial entrepreneur who has sold multiple mining companies for billions of dollars. His son Nikolas recently joined Norsemont as Director of Corporate Development. That’s not a passive investment. That’s a family betting on this story with both capital and careers.

Quinton Hennigh and Crescat Capital are on the register. Hennigh built his reputation identifying undervalued gold assets before the market catches on. Crescat didn’t just invest once. They increased their position at a higher price in December. When a sophisticated fund averages up, it tells you everything about their conviction level.

Victor Cantore of Amex Exploration is on the register. Larry Lepard, the macro-focused fund manager who has been pounding the table on gold, is on the register. Multiple European and American strategic investors participated in the recent $15 million raise.

Here’s what stands out. Norsemont Mining Inc. (CSE:NOM) (OTCQX:NRRSF) has raised over $21 million without a single broker or hedge fund involved. Every dollar came from investors that CEO Marc Levy personally knows and vetted. That’s almost unheard of in the junior mining space.

And speaking of Marc Levy, let’s talk about alignment.

Levy and his family trust have invested approximately $10 million into Norsemont. That represents roughly 21% ownership of the entire company. When did you last see a junior mining CEO with that kind of skin in the game?

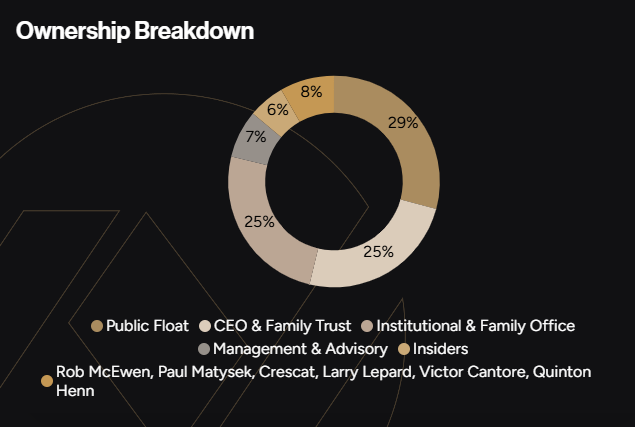

Add it all up and Norsemont Mining (CSE:NOM) (OTCQX:NRRSF) has approximately 38% of its shares held by insiders and strategic investors.

That’s an incredibly tight structure. It means limited selling pressure. It means the people closest to this story are believers. And it means when broader market attention arrives, there won’t be much stock available.

The 52-week range tells the story. The stock traded as low as C$0.18 and has reached as high as C$1.80. It’s moved, but it’s still trading well below highs while gold tests $5,000 once again.

Norsemont Mining Inc. (CSE:NOM) (OTCQX:NRRSF) isn’t a secret anymore. But it’s not crowded either. The smart money has positioned. The question is whether you recognize what they see before the rest of the market does.

The Math Doesn’t Add Up. Why This Stock Could Be Trading at a Fraction of What the Ounces Are Worth

Here’s where this story gets interesting for investors who pay attention to valuation.

The gold mining industry has a simple rule of thumb. Development-stage ounces in the ground are typically valued at $100 per ounce for companies with quality assets in good jurisdictions. Some trade higher. Some trade lower. But $100 per ounce is the benchmark that analysts and acquirers use as a starting point.

Norsemont Mining Inc. (CSE:NOM) (OTCQX:NRRSF) has 2.18 Million indicated and 557,000 inferred gold-equivalent ounces in the ground. At $100 per ounce, that implies a valuation of approximately $274 million.

The current market cap? Roughly $96 million.

That’s less than $40 per ounce for a past-producing asset with $175 million in existing infrastructure,29 a near-term production pathway, 80% of the resource in the indicated category, and a management team that has already built and sold billion-dollar mining companies.

The disconnect is glaring.

Now look at the comparable companies. Rio2 Limited operates in Chile mining gold at lower grades than Choquelimpie’s resource. Their market cap sits at $1.75 billion. They had to raise hundreds of millions in capital to build their operation. Norsemont Mining (CSE:NOM) (OTCQX:NRRSF) is targeting production with a tiny restart capex because the infrastructure already exists.

One company trades at a billion-dollar valuation. The other trades at $96 million. Both are permitted gold operations in Chile. The difference in valuation is difficult to justify once you understand what Norsemont actually controls.

And it’s not just the current resource that’s being ignored.

The market is assigning zero value to the resource expansion potential from 2.18 Million indicated and 557,000 inferred gold-equivalent ounces to 7.5 million to 9 million ounces.30 Zero value to the copper porphyry system sitting beneath the gold deposit. Zero value to the 210,000 ounces already sitting in stockpiles ready to be leached. Zero value to the silver credits that become increasingly meaningful with silver above $80.

When you look at the math, it’s hard to argue.

Valuation gaps like this don’t last forever. They close in one of two ways. Either the market wakes up and reprices the stock. Or a larger company writes a check and takes the asset out at a premium.

With Rob McEwen, Paul Matysek, Crescat Capital, and a dozen other sophisticated investors already positioned, the betting is that someone has already done the math. The question is how long before the rest of the market catches up.

At current prices, Norsemont Mining (CSE:NOM) (OTCQX:NRRSF) offers the kind of asymmetric setup that rarely lasts.

The Team Behind the Story. Billion-Dollar Track Records and the Operator Who Originally Built This Mine

Valuation gaps don’t close themselves. They close when execution happens. And execution requires the right people.

This is where Norsemont Mining Inc. (CSE:NOM) (OTCQX:NRRSF) separates itself from the pack of junior mining hopefuls. The team assembled here isn’t learning on the job. They’ve built mines. They’ve sold companies for billions. And one of them literally put Choquelimpie into production the first time around.

Marc LevyChairman and CEO

Marc LevyChairman and CEO Mijael ThielLead Mining Engineer

Mijael ThielLead Mining Engineer Dr. Sergei DiakovDirector

Dr. Sergei DiakovDirector David FlintChief Geologist

David FlintChief Geologist David LaingTechnical Advisor

David LaingTechnical AdvisorThis isn’t a team hoping to figure it out. This is a team that has done it before. Multiple times. At billion-dollar scale.

What’s Coming in 2026. A Stacked Calendar of Potential Catalysts That Could Force a Re-Rating

Junior mining stocks don’t move on hope. They move on news. And Norsemont Mining Inc. (CSE:NOM) (OTCQX:NRRSF) has one of the most catalyst-rich calendars in the sector heading into 2026.

Phase 3 Drilling Results (Q1 2026) — The company completed 7 deep diamond drill holes targeting 300 meters depth before pausing for weather in December. Assays are pending. These results will test the thesis that mineralization extends well below the 70-meter average of historical drilling. Positive intercepts could significantly expand the resource envelope.

Metallurgical Testwork (Q1-Q2 2026) — Cyanide-soluble gold analyses are in progress for stockpile and Phase 3 drill samples. These results will be utilized to select the materials for the column leach tests. This testing will be initiated in February.

Engineering Study (Q2 2026) — Detailed plant refurbishment scope, capex estimates, and production timelines will be released. This is when the market gets hard numbers on what it actually costs to restart Choquelimpie.

Updated Resource Estimate (Q2-Q3 2026) — Incorporating Phase 3 drilling results into a new NI 43-101 resource. If the depth extensions prove out, Norsemont Mining (CSE:NOM) (OTCQX:NRRSF) could be announcing a materially larger resource.

Preliminary Economic Assessment (Q3 2026) — The PEA will put formal economics around the oxide heap leach operation. Expect NPV, IRR, payback period, and production projections that give institutional investors the numbers they need.

Environmental Impact Assessment Submission (Q3-Q4 2026) — Filing the EIA triggers the government review clock and puts Norsemont Mining Inc. (CSE:NOM) (OTCQX:NRRSF) on a clear path to permitted production.

Six major catalysts. Twelve months. Each one capable of moving the stock.

The Window Won’t Stay Open Forever. Here’s How to Learn More Before the Market Catches Up

The setup here is rare.

A past-producing gold mine with 2.18 Million indicated and 557,000 inferred gold-equivalent ounces in the ground. $175 million in existing infrastructure that compresses the timeline and capex. A realistic path to production in 2027. Resource expansion potential to 7.5 million ounces or more. A copper porphyry system at depth that hasn’t even been factored into the valuation. Billionaire investors and legendary mine builders already on the register. A CEO with $10 million of his own money in the deal.

And all of this trading at less than $40 per ounce while gold is pushing back towards $5,000.

Norsemont Mining Inc. (CSE:NOM) (OTCQX:NRRSF) is not a secret. The smart money has found it. But it’s not crowded yet. The company is only now beginning to tell its story more broadly, and 2026 is shaping up to be the year that changes the narrative entirely.

Valuation gaps like this close fast once the market pays attention. Catalysts are stacked. Execution is underway. The macro backdrop for gold hasn’t been this favorable in decades.

The question isn’t whether this story deserves a closer look. The question is whether you’ll take that look before or after the re-rating happens.

Download the investor presentation here to get the full technical breakdown, drill results, and management commentary.

Norsemont Mining (CSE:NOM) (OTCQX:NRRSF) — One of the most asymmetric setups in the gold sector heading into the best gold market in 50 years.

*All prices in USD unless otherwise stated