On May 2, 2026, Spirit Airlines collapsed. Tens of thousands of passengers were stranded with no seats left on competing carriers and collapsing customer service lines.1

That same week, residents in Memphis were fighting a new water-and-power-hungry AI data center. A recent Gallup poll found 71% of Americans now oppose new AI data centers in their communities.2

Somewhere else, a patient is back in the ER for the third time this month, in serious pain. The surgery that would fix them is being blocked by an insurance administrator’s checklist and all those ER visits, scans, and delays will end up costing far more than the surgery ever would have.3

Three industries. One shared root cause. Legacy systems were not built for the AI era, and bolting AI onto them is not working.

These are not isolated failures. They are the visible edges of a much larger shift. The AI economy is splitting into specific battlegrounds. Four of them are distributed inference compute. Surgical healthcare cost. Real-time travel disruption. Content discovery. Each one carries trillion-dollar stakes. Each one needs an AI-native solution, not an AI-bolted-on patch.

Most public AI plays are single-vertical. One product. One market. One risk.

The exception is a Nasdaq-listed company called Auddia Inc. (NASDAQ:AUUD). It currently trades at a tiny market cap of under $10 million.

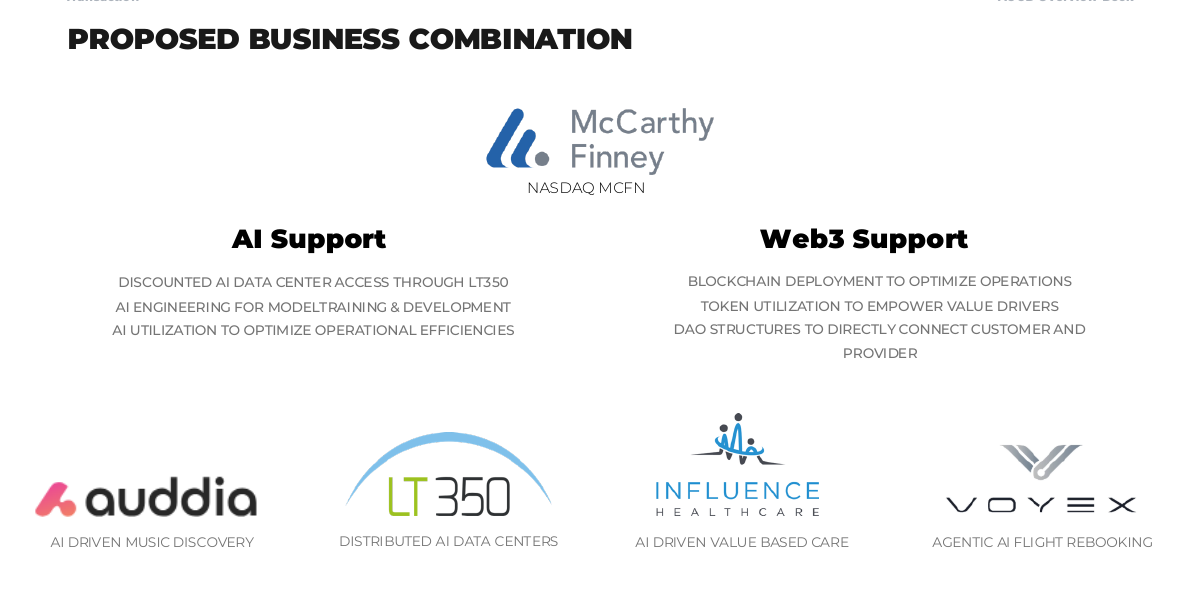

On May 15, 2026, the company filed a Form S-4 with the SEC to merge with Thramann Holdings, LLC, and re-list under a new holding company called McCarthy Finney, Inc. (NASDAQ: MCFN).4

The new entity will own four AI operating subsidiaries solving exactly those four pain points. All four share one operating system, one engineering bench, and one infrastructure layer. The base case discounted cash flow valuation disclosed by management is approximately $250 million.5 Independent investment bank Houlihan Capital, LLC has issued a written fairness opinion concluding the merger consideration is fair from a financial point of view to Auddia stockholders.

Investors who follow reverse mergers know the value gap does not close at deal announcement. It closes between S-4 filing and shareholder vote.6 That window just opened.

What Auddia Is About To Become, In Plain English

Picture a parent company that owns four small AI-powered startups. The parent gives each startup three things. Cheap access to its own private data center network. A shared bench of AI engineers. A common operating system that handles the back-office work.

Each startup focuses on solving one big real-world problem. None of them has to build the AI infrastructure from scratch. None of them has to hire its own engineering team. None of them has to figure out billing or security or compliance alone.

The parent will be called McCarthy Finney. The name pays tribute to John McCarthy, the father of artificial intelligence, and Hal Finney, an early digital currency pioneer. Today it trades under the Auddia ticker as AUUD. After the merger closes, it will trade as MCFN on Nasdaq.8

The four subsidiaries each tackle one trillion-dollar problem.

LT350 turns parking lot airspace into distributed AI data centers, addressing the land, power, water, and community-opposition constraints throttling traditional AI infrastructure. The architecture requires no new land use, consumes zero water (closed-loop cooling), and deploys at the circuit level without transmission upgrades at a time.9

Influence Healthcare uses AI to replace the 20-administrators-per-doctor overhead that has put corporations, not clinicians, in charge of medical decisions. The result: doctors and nurses make the calls again and are recognized for delivering higher-quality care at lower cost.10

Voyex is building FlightFix, an agentic AI platform that will monitor itineraries and automatically rebook travelers before disruptions strand them. The product was unveiled in response to the Spirit Airlines shutdown that left tens of thousands of passengers without options; an MVP is targeted for ~6 months after merger close.11

Auddia Inc. (NASDAQ:AUUD) gives independent artists guaranteed plays inside real AM/FM station streams via its faidr app, tackling radio’s discovery problem. 12

Each subsidiary has standalone upside. Together, they share McCarthy Finney’s Operating System and LT350’s discounted data center capacity. That is how four small AI companies become one platform worth far more than the sum of the parts.

The Holding Company: McCarthy Finney

This is not a passive holding company. It is an operating platform.

McCarthy Finney will run an AI-native shared platform called the McCarthy Finney Operating System, or MCFN-OS.13 MF-OS gives each subsidiary four shared services: centralized AI engineering, workflow automation tools, cross-vertical data and model learning infrastructure, and identity/permissions/audit frameworks. McCarthy Finney is also positioned as a delivery layer for “AI and Web3 services” to its four portfolio companies.

Why this matter? Most legacy companies adopting AI agents have to rip out existing systems and retrain the people running them. McCarthy Finney is starting from zero. Every subsidiary is being built AI-native from day one.

The deal structure is straightforward. Thramann Holdings, , the private company that owns LT350, Influence Healthcare, and Voyex, will combine with Auddia Inc. (NASDAQ:AUUD) to form McCarthy Finney (NASDAQ: MCFN), with all four operating companies as subsidiaries. At closing, Auddia stockholders are expected to own approximately 20% of the combined company; Jeff Thramann will own approximately 80%.

That 20% stake represents pro-rata exposure to roughly $50 million of management’s base-case DCF valuation of $250 million for the combined entity. The current Auddia standalone market cap sits under $10 million. $10 million of pre-merger cap converts into a stake in roughly $50 million of post-merger value if management projections approximate reality. That gap is the re-rate setup.

The $12 million cash-on-hand closing condition has already been satisfied. Auddia Inc. (NASDAQ:AUUD) raised approximately $12.9 million year-to-date through April 29, 2026 to meet the cash test.14 That removed the single biggest execution risk in the deal. The only remaining gates are SEC review of the S-4 and the shareholder vote.

Subsidiary 1: LT350. Turning Parking Lots Into AI Data Centers

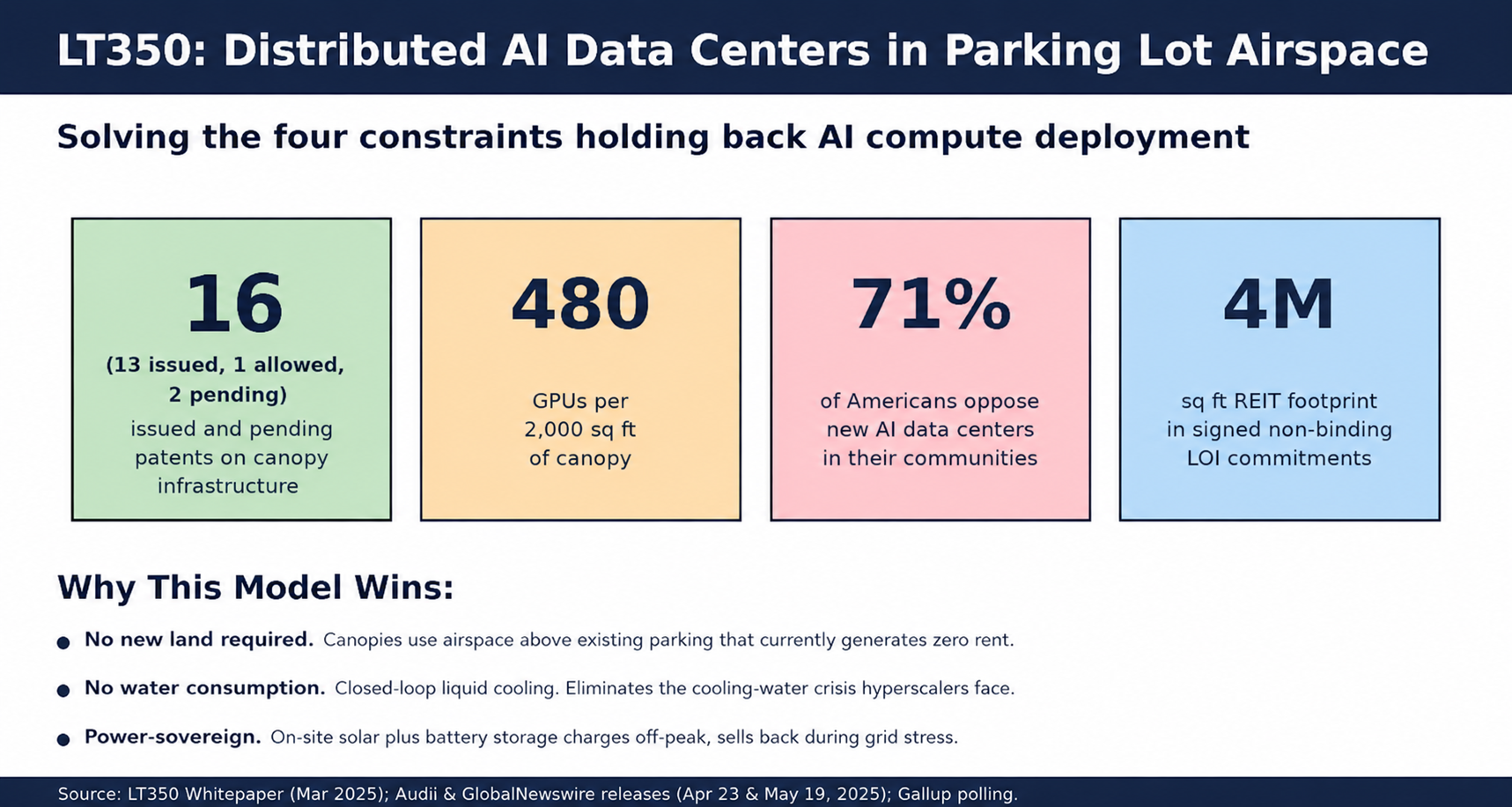

LT350 accounts for roughly 50% of the internal DCF valuation.15 It is the biggest piece. It solves the single biggest constraint in the AI economy: where do you actually put the data centers?

AI compute demand is exploding. But 71% of Americans now oppose new AI data centers being built in their communities.16 Grids are buckling under load. Water restrictions are tightening. New megacenters take years to permit and interconnect.

LT350’s answer is elegant. Build the AI data center into solar canopies that sit over existing parking lots.

No new land is needed. The canopies sit in airspace that currently does nothing. Solar panels on top, paired with battery storage, provide most of the power. The compute cartridges are water-cooled in a closed loop, so there is no ongoing water consumption. The whole system sits behind the meter and can disconnect from the grid during peak demand.

As Auddia Inc. (NASDAQ:AUUD) CEO Jeff Thramann has framed it, the model is engineered to deploy AI infrastructure that fits inside the footprint of the world we have already built.17

LT350 holds 14 allowed and 2 pending patents covering canopy structure, modular GPU and battery and memory cartridges, closed-loop cooling, mesh connectivity, and mobility-and-logistics integration.18 The patent portfolio is the moat.

The system is designed for inference workloads, not training. Training happens overnight in giant centers far from anywhere. Inference has to happen close to where the data is generated. Hospitals. Autonomous vehicles. Defense facilities. Financial trading floors.

LT350 already has commercial validation. A non-binding letter of intent with a NYSE-listed medical REIT gives LT350 access to roughly 4 million square feet of suitable parking lot airspace across approximately 200 medical facilities.19 The first pilot is targeted for a hospital property in the Dallas-Fort Worth area.

The capacity math is straightforward. Each canopy supports 480 GPUs per 2,000 square feet of canopy space.20 Scaled across a single REIT footprint, that adds up to a serious amount of compute deployed in months instead of years.

How The Market Has Priced Similar Stories

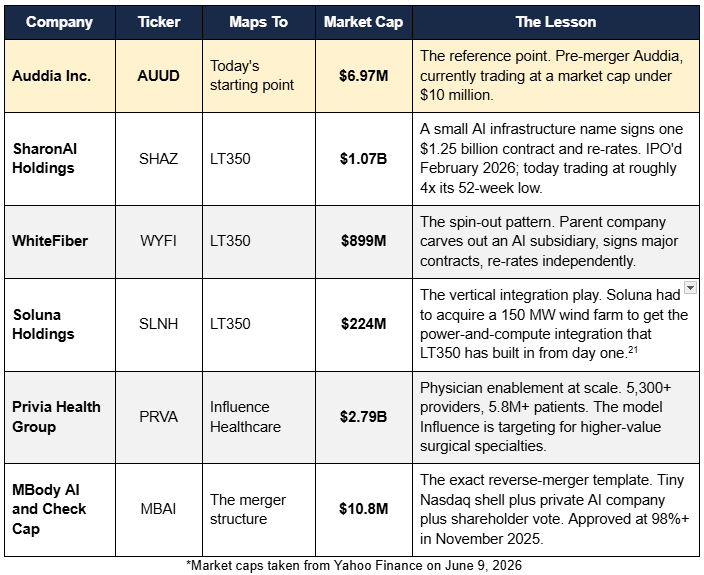

To understand what Auddia Inc. (NASDAQ:AUUD) and McCarthy Finney could become, look at the names that have already walked this path.

Each one started as a small or specialty-focused stock and grew into the AI infrastructure or value-based care conversation. None of them had a four-vertical structure. None of them had LT350’s combined land, power, and patent advantages from day one. Every one of them got there by signing one credible contract.

The pattern across these comps is consistent. Start small. Sign one credible contract or partnership. Watch the market re-rate the equity to reflect the new opportunity rather than the old shell.

SharonAI Holdings is the cleanest example. The company listed publicly in February 2026, signed a $1.25 billion five-year AI cloud agreement weeks later,22 and today carries a market cap of over $1 billion. WhiteFiber tells the same story from a spin-out angle, locking in an $865 million 10-year colocation contract23 and now trading near $1.21 billion.

Soluna Holdings is the most instructive comparison. To get the integrated power-plus-compute model that LT350 has by design, Soluna had to acquire a 150 megawatt wind farm for $53 million and bolt it onto their data campus.24 LT350 has the same integration baked in from the canopy up.

Privia Health Group anchors the healthcare leg. At a $2.79 billion market cap, with 5,300 physicians and 5.8 million patients on the platform,25 PRVA shows what physician enablement looks like when it scales. Influence Healthcare is going after the higher-cost surgical specialty layer that PRVA’s primary-care model does not directly address.

MBody AI’s reverse merger into Check-Cap is the structural proof. The exact playbook Auddia Inc. (NASDAQ:AUUD) is running closed in November 2025. Shareholders approved that transaction at over 98%.26

None of these comparables is a guarantee. Each one carries execution risk. Market caps shown here are point-in-time snapshots that can move sharply in either direction. The takeaway is that the path from microcap shell to credible AI platform has been walked, and the pattern is recognizable.

Press Releases

Subsidiary 2: Influence Healthcare. Putting Surgeons Back In Charge Of Surgical Care

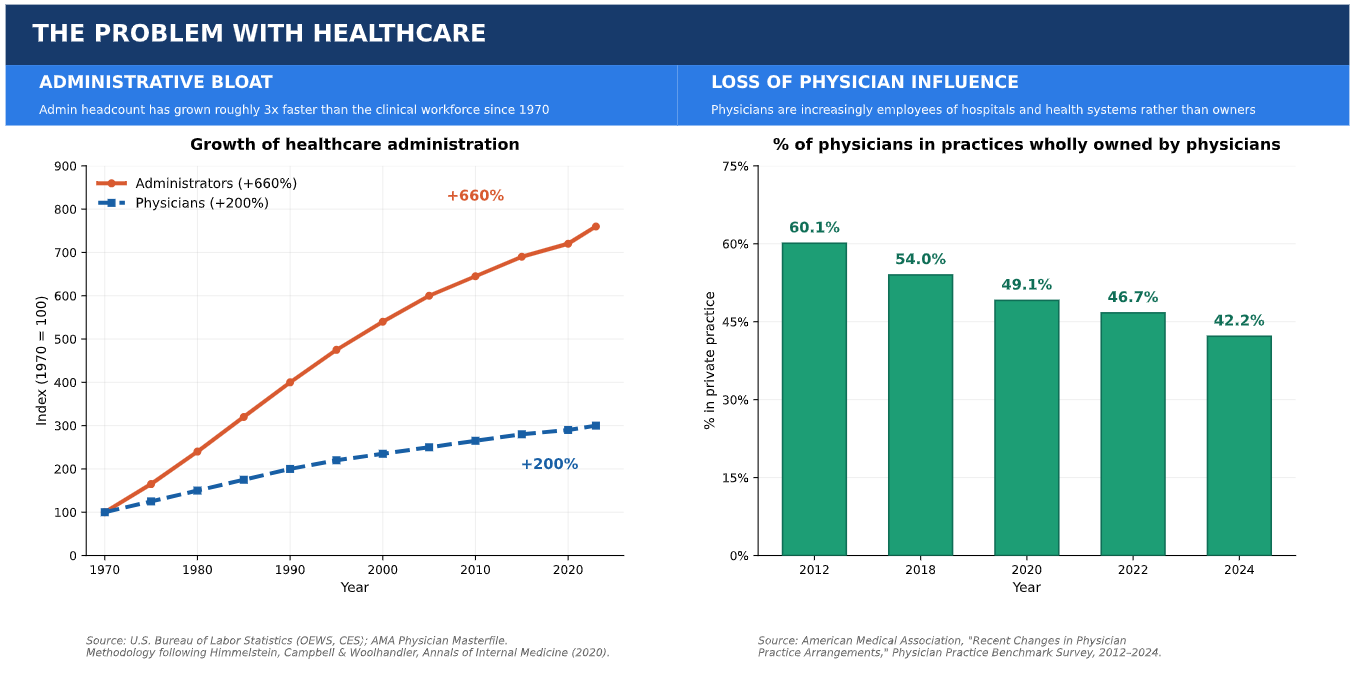

Two structural problems weigh on surgeons today.

Their clinical judgment is increasingly overridden by administrators and checklists, eroding the autonomy that drew most of them into medicine.

And the work of actually driving the cost out of a surgical episode (choosing the right implant, eliminating unnecessary imaging, cutting wasted steps), sits with the surgeon, the one person in the room who is not structurally recognized for doing it. The people best positioned to deliver better care at lower cost have neither the freedom to make those calls nor a mechanism that rewards them for the extra work it takes.

Influence Healthcare operates through a regulatory category called a Value-Based Enterprise, or VBE, to let surgeons participate in those profits.27 The mechanic is straightforward. Vertically integrate the hospital, the implants, and the imaging into a single bundle. Target roughly 50% off the standard surgical cost. Recognize the surgeons who deliver higher-quality outcomes at lower cost with increased compensation for the work required to make that happen.

Why this works where previous value-based care (VBC) models have struggled. Only surgeons can lower cost without lowering quality. You cannot checklist your way to better surgery from an administrator’s office. The person holding the scalpel is the only one who can decide which implant is good enough, which imaging is necessary, and which step is wasted motion. That work is real, it is hard, and it requires surgeons to engage with the case in ways the current system does not ask of them.

For patients, the model means decisions made by doctors based on knowledge, not by administrators based on checklists. For surgeons, it means the freedom to practice medicine without the friction of irrelevant administrative overhead, with appropriate recognition and compensation for the additional work that delivering higher-quality care at lower cost requires.

The market entry is spine and orthopedic surgery, expanding to all surgical specialties across the top 100 metropolitan statistical areas.

The tailwinds are real. McKinsey projects specialty-care revenue will grow 4–5% annually from 2024 to 2029, with care delivery continuing to shift from acute hospitals to ambulatory surgery centers. Influence Healthcare targets both. ASCs already give surgeons a meaningful operational role. Hospitals, where the most complex and highest-value cases will always be done, have historically lacked an equivalent model. Influence Healthcare is designed to extend a surgeon-led model into that setting.

Tie this back to Privia Health Group on the comp table. PRVA built a $2.79 billion enterprise on physician enablement for primary care. Influence Healthcare targets the higher-value surgical specialty layer above it. The same VBE rules that legalize Influence Healthcare’s model now also allow primary care VBC platforms and surgical VBEs to share profits across a bundled care episode.

That cooperation was not allowed before. It is now.

The implication: the largest primary care VBC players, like Privia, Amazon Health, CVS Health, and ChenMed, become potential distribution partners rather than competitors.28 Each one can route surgical case volume into Influence Healthcare’s network at scale. Right now, the only way public investors can get exposure to this is through Auddia Inc. (NASDAQ:AUUD) ahead of the McCarthy Finney merger.

Surgery is where the largest savings opportunity sits, and where the impact on patient care is highest.

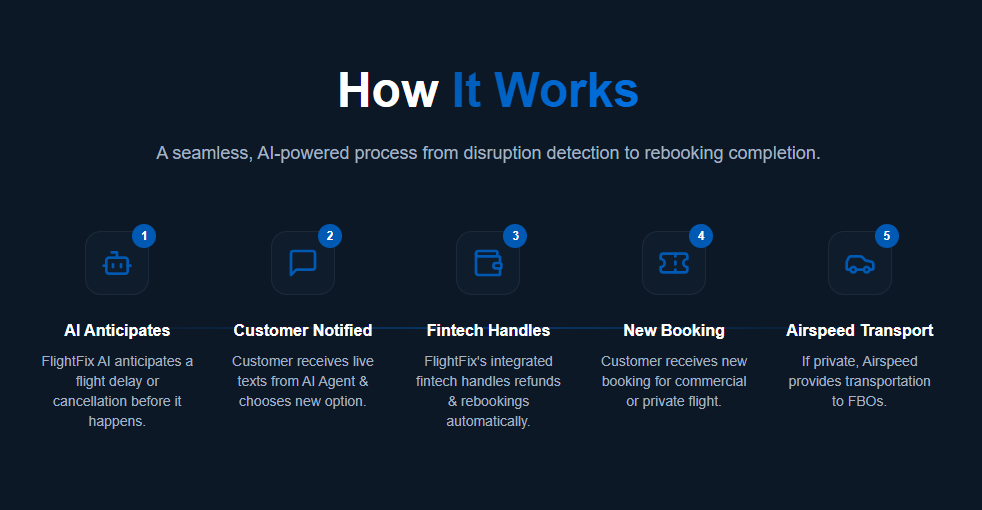

Subsidiary 3: Voyex. Stopping The Spirit Stranding From Happening Again

Voyex was built for exactly the kind of chaos that hit American air travel in early May 2026.

When Spirit Airlines shut down, it became the first major US carrier in 25 years to go out of business due to financial problems,29 stranding thousands of passengers across the country and forcing Southwest alone to absorb more than 20,000 of them in a single day. Spirit cancelled all flights, told customers not to come to the airport, and shut down its own customer service entirely.

Voyex’s flagship product is called FlightFix. It is an agentic AI travel assistant that runs in the background of your trip.

FlightFix will watch your itinerary in real time, predict delays and cancellations before they hit and pre-buy refundable seats on alternate flights when it sees one coming. By the time your original flight is officially cancelled, you have already received a text message with a new boarding pass.

The premium feature is what happens when commercial seats run out, which is exactly what happened during the Spirit collapse. FlightFix is being architected to aggregate stranded passengers and shuttle them to contracted private jets and charters through fixed-base operators (FBOs). A Voyex-branded van picks members up at their gate and drives them across the tarmac. They board a private aircraft and continue on their way.

The subscription is expected to be priced at approximately $199 per year, similar to a CLEAR or Global Entry membership. Most members will never use the private jet rescue feature. Those who do will get rescued at a fraction of the cost of self-booking a charter. The economics work because only a small percentage of trips actually need the rescue.

FlightFix is targeted for MVP launch approximately six months after the Auddia Inc. (NASDAQ:AUUD) merger closes.30 The fintech clearing layer that handles refunds, credits, and rebookings is being built on the McCarthy Finney shared operating system.

Source: Voyex Overview Deck citing Statista, IBISWorld, Allied Market Research, U.S. Bureau of Transportation Statistics. Combined addressable market across legacy travel agencies, OTAs, and corporate travel management.

What sets FlightFix apart is the combination of three elements that do not currently exist in one product anywhere in the market. Predictive rebooking before the cancellation is announced. A private jet rescue path through FBO partnerships when commercial seats run out. And a fintech clearing layer that handles refunds, credits, and rebookings automatically through the McCarthy Finney shared operating system.31 Together they address the exact failure mode the Spirit shutdown exposed.

Subsidiary 4: Auddia. The Original Business, Now With Traction

Auddia Inc. (NASDAQ:AUUD) is the legacy business that originally went public five years ago. It is AI applied to AM and FM radio. It is also the subsidiary where the new business model is starting to produce real data.

Two products carry the business. faidr is a consumer app that streams any AM or FM radio station with the commercials automatically removed. The AI replaces the ad breaks with curated music from up-and-coming artists. Discovr Radio is the B2B platform where independent artists and small labels pay to get their tracks placed inside those streams.

The pivot is the story here. Auddia Inc. (NASDAQ:AUUD) spent five years trying to build a consumer subscription business and never reached scale. In Q1 2026 the company flipped to a B2B model where independent artists pay subscription fees for guaranteed exposure to real radio audiences. Artist subscriptions are priced at approximately $250 per year.

The early traction is meaningful. Discovr Radio launched in MVP form on January 20, 2026. According to Auddia‘s May 21, 2026 disclosure, the platform has logged more than 100,000 plays of Discovr artists’ songs, established nearly 1,000 artist and label accounts, and is generating a 44% average click-through rate on artist profile pages with a 30% conversion rate from free to paid customer. Participating artists are averaging roughly 116 plays per week on live AM/FM streams.33

The market is large enough to matter. There are roughly 60 million US radio streamers, 1.7 million new artists tracked annually, and approximately $1.5 billion spent by non-major labels marketing their artists in 2023.34 A single-digit market share of label marketing spend would re-rate Auddia Inc.’s (NASDAQ:AUUD) standalone economics meaningfully.

Why Now. The Catalyst Calendar

Reverse merger investors know the value gap closes during a specific, dated window. For Auddia Inc. (NASDAQ:AUUD), that window opened on May 15, 2026 with the S-4 filing.35 Here is how the rest of the calendar runs.

Step 1: SEC comments on the S-4. Standard SEC review timeline runs 30 to 45 days for first comments.36 During that window the company refines its disclosures and addresses regulator feedback.

Step 2: Proxy launch and shareholder vote. Once the SEC clears the S-4 as effective, a 25-day proxy window opens. Shareholders of record vote on the merger. The transaction is targeted to close in Q3 2026.

Step 3: The ticker change to MCFN. Auddia Inc. (NASDAQ:AUUD) rebrands as McCarthy Finney. The four-subsidiary structure becomes the operating reality.

The biggest gating risk in the deal has already cleared. The merger agreement requires $12 million in cash at closing,37 and AUUD locked that in with a $12 million public offering priced at $2.36 per share, closing three days later.38 All in, the company has secured roughly $12.9 million in financing year-to-date. Both boards have unanimously approved the deal.39 The financing risk is off the table. What’s left is SEC clearance of the S-4 and a shareholder vote, both on the standard reverse-merger track.

As part of the S-4 filing, an independent third-party investment bank rendered a written fairness opinion concluding that the merger consideration to be received by Auddia Inc. (NASDAQ:AUUD) stockholders at the time of signing the merger agreement is fair from a financial point of view. The opinion and the firm’s identity are disclosed in the S-4 itself.

Market response has been visible. Volume spiked sharply on the merger announcement, on the 14th patent allowance for LT350, and on the S-4 filing. On the day of the S-4 filing alone, Auddia Inc. (NASDAQ:AUUD) trading volume reached approximately 135 million shares. That kind of volume in a sub-$10 million market cap stock is the market actively pricing in the merger optionality.

Capital Stack and Deal Structure Snapshot

6 Reasons

Auddia (NASDAQ:AUUD) Deserves A Spot On Your Radar Right Now

1

The Valuation Gap Is Stark. Management’s base case DCF for McCarthy Finney is approximately $250 million. Auddia Inc. (NASDAQ:AUUD) trades at a market cap under $10 million today. Even a meaningful fraction of the DCF being realized in market value would represent a substantial re-rate.

2

The Catalyst Window Is Short And Dated. SEC comments typically arrive 30 to 45 days after S-4 filing. The proxy and shareholder vote follow within roughly 60 to 90 days after that. Investors who follow reverse mergers know this window concentrates a series of catalysts: SEC comment resolution, definitive proxy mailing, shareholder vote, and closing.40

3

LT350 Alone Could Justify The Story. SharonAI Holdings trades at a $1.11 billion market cap. WhiteFiber trades at $1.21 billion. Neither has LT350’s combined land, power, water, and patent advantages. If LT350 lands one comparable contract, the math gets interesting fast.

4

The Founder Has Done This Five Times Before. Jeff Thramann has built and exited five companies. LANX, ProNerve, US Radiosurgery, American Physicians, and Rocky Mountain CyberKnife. Three of those exits alone totaled $223 million.41 He is a named inventor on more than 130 US and international patents.42 The same operating playbook is running here.

5

The AI Inference Tailwind Is Structural, Not Cyclical. Edge inference is moving compute closer to where data is generated. Hospitals. Autonomous vehicles. Defense facilities. Financial trading floors. Regulators are increasingly pushing AI loads to bring their own power. LT350’s power-sovereign architecture aligns with both trends simultaneously.

6

Four-Vertical Optionality Multiplies Outcomes. Any single subsidiary breaking out would re-rate the whole stack. LT350 lands a marquee contract, re-rate. Influence Healthcare signs its first integrated surgical bundle, re-rate. Voyex launches FlightFix and gets one viral disruption moment, re-rate. Investors are paying for one platform but holding optionality across four independent paths to upside.

Risks, Frankly

No investment thesis is complete without an honest accounting of what could go wrong. Here is what could.

Three of the four subsidiaries are pre-revenue. LT350, Influence Healthcare, and Voyex are all in development or early commercial stages. The internal DCF valuation depends on projections, not realized results.

McCarthy Finney will be a Nasdaq-defined controlled company. Jeff Thramann is expected to control approximately 80% of the voting power following close. That gives him broad authority over matters submitted to a stockholder vote, including the election of directors. Auddia Inc. (NASDAQ:AUUD) stockholders end up with approximately 20% of economic interests. The math favors current AUUD holders only if the DCF valuation is materially closer to $250 million than the current standalone market cap. That outcome depends on execution.

The merger is still subject to SEC review and shareholder approval. Either could be delayed or modified. Auddia is required to maintain at least $12 million in cash at closing as a condition precedent, though Auddia and Thramann can waive this requirement by mutual agreement.

Auddia’s B2C to B2B transition is still early. Discovr Radio launched in MVP form on January 20, 2026. The 116 plays per week and 44% click-through rate are encouraging signals but have not yet translated to material revenue.

Microcap volatility is real. AUUD has historically traded with elevated volatility. Both upside and downside moves can be sharp.

Discounted cash flow valuations are projections, not promises. The numbers cited above reflect management’s internal base-case assumptions. The Houlihan fairness opinion addresses the fairness of the merger consideration at signing, not the realization of the DCF projections.

Past performance of comparable companies does not predict future performance of Auddia Inc. (NASDAQ:AUUD) or McCarthy Finney. Investors should review the full risk factors disclosed in the company’s SEC filings, including the S-4 registration statement filed May 15, 2026.

The People Behind The Platform

A founder with five prior exits, a CFO who has operated through SEC reporting at scale, and an independent board built specifically for AI infrastructure, capital structuring and digital-asset oversight. The bench was assembled for this transaction, not retrofitted to it.

The Bottom Line

Auddia Inc. (NASDAQ:AUUD) is a sub-$10 million Nasdaq-listed company approximately 60 to 90 days away from becoming McCarthy Finney (NASDAQ: MCFN). A four-subsidiary AI conglomerate with a $250 million base case DCF, a Houlihan Capital fairness opinion, and a Q3 2026 close target.

The setup combines a short-duration catalyst window, a de-risked financing condition that has already closed, Houlihan Capital issued an independent third-party fairness opinion, and a four-vertical platform structure that gives the equity multiple independent paths to upside.

The SharonAI, WhiteFiber, Soluna, Privia Health, and MBody AI comparisons all point in the same direction. Small AI platforms with credible technology and one good contract re-rate sharply. Reverse mergers from microcap shells into purpose-built AI operating companies have closed at 98% shareholder approval in the last six months. The path exists. It has been walked.

For investors who follow special situations, reverse mergers, and small-cap AI infrastructure, Auddia Inc. (NASDAQ:AUUD) is worth a spot on the radar before the proxy window closes.

The window is open. It does not stay open forever.

Subscribe here to download their latest Corporate Presentation.